Michael & Julie - age 59 & 54

Michael is the founder and 50percent shareholder of a Sydney-based consulting company, while Julie is the admin manager. They receive income of $250,000 per annum from wages, and dividends from the business. They are in good health and enjoy an active lifestyle that is focused on their children and grandchildren. Financial security is important and they “hope that we have enough assets to maintain our lifestyle in retirement”.

Assets and Mortgages

They reside at Rose Bay, and have investment properties at Darling Point, Maroubra and Avoca Beach. The properties are worth $7.7m, while they have mortgages of $3.5m. They have recently purchased a quality apartment at Darling Point and they are selling the Avoca Beach apartment to reduce debt. Their other assets include a small cash reserve in their working account, super of $583k, shares of $57k, a boat worth$300k, and equity in the business of $500k.

Retirement Plan

Michael has indicated that he will likely retire at age 65 in five years. At that he would like to retire all debt, and have assets producing an income stream to meet their living needs of$20,000 per month. Michael realises that he will have to sell his boat at retirement as the running costs will absorb too much of their cash flow should he keep it. They also own 50% of a commercial office in Sydney CBD, and at retirement their half share should net them a

monthly income of $6,733. The Maroubra unit should net $1,030 per month by 2025. They are thinking at retirement of selling their Rose Bay home and using the proceeds to pay out mortgages, and then move into their Darling Point apartment, which has magnificent views of Sydney harbour.

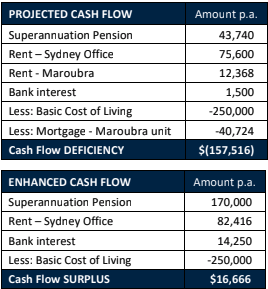

Financial Analysis

We projected Michael and Julie’s assets out over the next five years should they continue on their current path.We estimated that once they had sold their Rose Bay home, sold their equity in the business, and used the proceeds to pay down their mortgages, that they would have an unencumbered apartment at Darling Point,

while the Maroubra unit should be worth $1.1m and have a residual mortgage of $352k. Their super would accumulate to $875k which should produce an income stream of $3,645 per month ,indexed by CPI. The

shares should increase in value to $79k, and they would have roughly $100k in bank accounts. At retirement their main income-producing assets will be the Sydney office, the Maroubra unit and super. The Sydney office should provide them with a monthly income of $6,300 net of expenses, while the unit should produce monthly net

rent of approximately $1,030.We anticipate that under Michael and Julie’s current retirement plan their cashflow

should be as shown in the top right table. Despite accumulating significant assets by their retirement in five

years, they will not produce the income that they require to maintain their current standard of living. In fact, we anticipate that they will have a significant shortfall of approximately$13,000 per month that will only worsen as

the years progress.

Strategic Advice

We prepared a Retirement Roadmap for Michael and Julie that provided seven-step strategic advice for them to implement over the next five years.The advice focused on paying down debt and increasing super contributions. With the same asset growth and return assumptions, we project that they should accumulate $10 million in unencumbered assets. Their super should be $1.9m at retirement.Despite drawing down $902k in the first 5 years

of retirement, with an additional$1m contributed from the sale of Rose Bay and the practice during these years, they should still have a balance of more than $2.8m in super when Julie reaches age 65.

By following our strategic advice over the next five years, we estimate that their cash flow will be as shown in the second table above.

Their super pensions will be tax free and by utilising their family trust they should have no tax on their other income. By following our strategic advice, Michael and Julie should have a monthly income stream of $22,000 to provide for their living needs. Michael andJulie are relieved that they will be able to maintain their existing lifestyle throughout their retirement. Michael is also very happy that he will be able to continue to afford to enjoy his boat for many years to come.

Disclaimer: This informationis general advice only, & has been prepared without taking into account theobjectives, financial situation, or needs of any individual. It is not aspecific recommendation to buy, sell or hold any product or security. Readers shouldseek financial advice before making a decision & should consider the appropriatenessof this advice in light of their own objectives, financial situation, &needs.